Fill out the form below and a specialist will be in touch shortly

A specialist will be in touch with you shortly.

Call Now: (877) 269-1339

What's in this guide

- How Structured Settlements Work?

- Common Types of Structured Settlements

- Structured Settlement Payment Options

- Advantages of Structured Settlements

- Disadvantages of Structured Settlements

- Legal Structure of Structured Settlements

- Can You Sell a Structured Settlement?

- How Selling a Structured Settlement Works

- Tax Implications of Selling a Structured Settlement

- History of Structured Settlements in the United States

- Frequently Asked Questions

- Conclusion

A structured settlement is a legal compensation arrangement in which an injured party receives payments over time rather than a lump-sum payment.

These settlements usually arise from civil lawsuits. Personal injury claims, medical malpractice cases, wrongful death suits, and workers’ compensation disputes commonly result in structured settlements. One party agrees, or is legally required, to compensate another party for harm caused. That compensation does not always arrive at once.

Structured settlements are typically agreed upon during negotiations, though courts can also order them as part of a judgment. Both sides usually participate in deciding how compensation will be paid. Smaller settlement amounts may result in lump-sum payments. Larger awards often move toward a structured format.

Once the settlement terms are finalized, the paying party funds an annuity through a life insurance company. This annuity guarantees payments according to a fixed schedule. Payments may arrive monthly, annually, or in increasing amounts over time, depending on the agreement.

The settlement contract defines the payment amounts, timing, and duration. Those terms remain locked in once the agreement is signed. Because the payments are guaranteed and legally binding, structured settlements provide predictable compensation rather than immediate access to the full award.

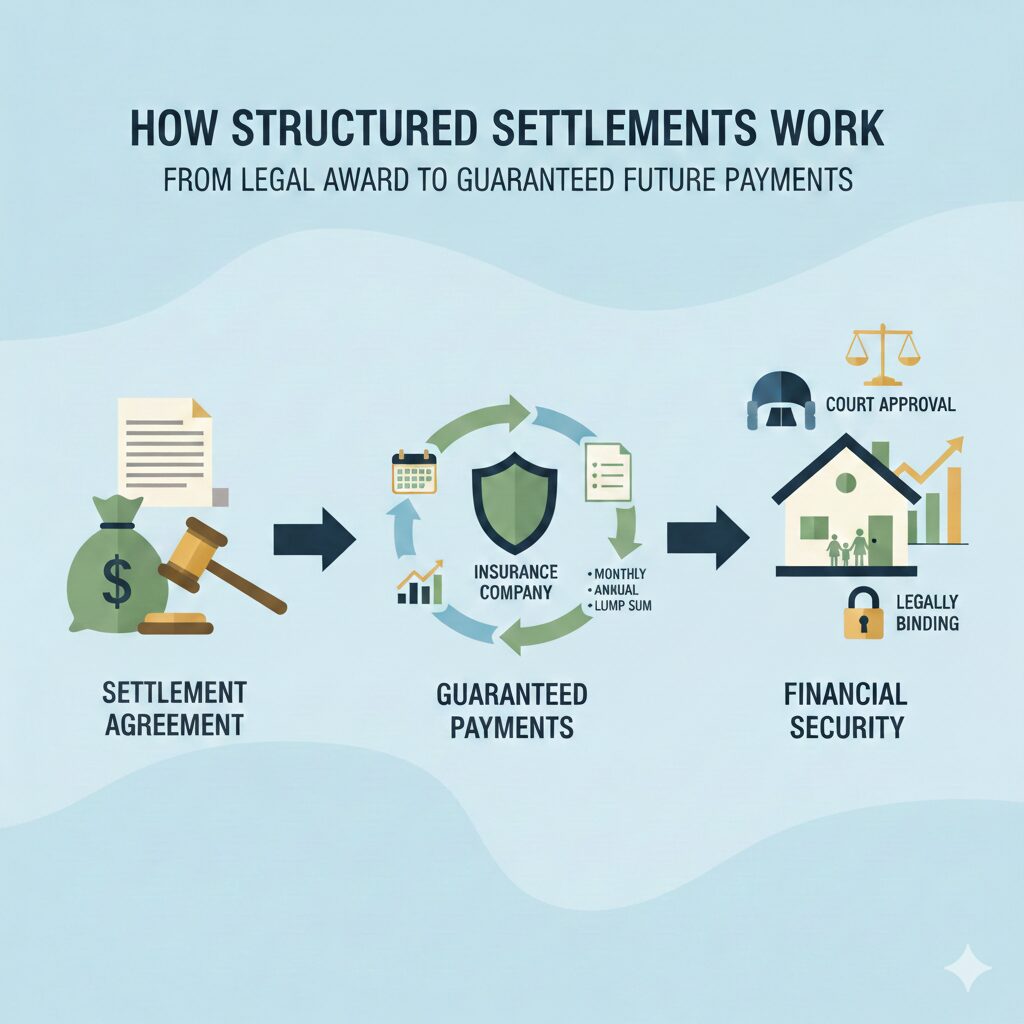

How Structured Settlements Work?

Structured settlements follow a defined legal and financial process. Every step is designed to convert a legal award into guaranteed payments over time. The structure remains fixed once approved, which removes uncertainty for both parties.

Structured settlements follow a defined legal and financial process. Every step is designed to convert a legal award into guaranteed payments over time. The structure remains fixed once approved, which removes uncertainty for both parties.

How Payments Are Created

The process begins after a settlement or court judgment determines the amount of compensation. Instead of paying the full amount directly to the injured party, the responsible party agrees to fund a payment schedule. That schedule outlines how much money will be paid, how often payments will be made, and for how long they will continue.

Payment structures vary. Some agreements provide a monthly income. Others offer annual payments or payouts that increase on specific dates. Certain settlements also include future lump sums for known expenses. Every detail is set out in the settlement contract and cannot be changed later without court approval.

The Role of Insurance Companies

Insurance companies play a central role in structured settlements. After the payment schedule is finalized, the defendant or insurer buys an annuity from a life insurance company. This annuity works as the funding body for the settlement.

The insurance company guarantees each payment as per the agreed schedule. Payment obligations do not depend on market performance or investment returns. Even if the original paying party faces financial trouble, the annuity issuer remains responsible for making payments.

This structure transfers long-term payment responsibility from the defendant to a regulated financial institution.

Why Courts Approve Structured Settlements

Courts approve structured settlements to protect recipients and ensure financial stability in the long run. Judges review settlement terms to confirm fairness, clarity, and compliance with applicable laws. However, approval becomes mandatory in cases involving minors or legally incapacitated individuals.

Court oversight also ensures payments serve the intended purpose of the settlement. Structured payouts reduce the risk of mismanagement and provide predictable compensation over time. Once approved, the settlement terms become legally binding and enforceable.

This combination of legal oversight, guaranteed funding, and fixed payment schedules explains why structured settlements are widely used in high-value personal injury and wrongful death cases.

Cash Your Structured Settlements With MySettlement

Common Types of Structured Settlements

Structured settlements apply to several legal situations. Each type follows the same core framework but serves a different purpose, depending on the nature of the claim and the recipient’s long-term needs.

Personal Injury Structured Settlements

Personal injury structured settlements arise from accidents that cause physical or psychological harm. These cases often involve auto accidents, premises liability, or product defects. Payments are designed to support medical care, rehabilitation, lost income, and long-term living expenses through a predictable payout schedule.

Medical Malpractice Structured Settlements

Medical malpractice structured settlements result from negligence by healthcare providers. Claims may involve surgical errors, misdiagnosis, or birth-related injuries. Settlement payments typically address ongoing treatment, therapy, assistive care, and future medical costs that may extend over decades.

Wrongful Death Structured Settlements

Wrongful death structured settlements compensate surviving family members after a fatal incident caused by negligence or misconduct. Payment structures often replace lost income, cover funeral expenses, and provide long-term financial support for spouses or dependents affected by the loss.

Workers’ Compensation Structured Settlements

Workers’ compensation structured settlements resolve claims related to job-related injuries or occupational illnesses. Payments typically cover wage replacement, permanent disability benefits, and future medical care. Structured payouts help injured workers maintain income stability after returning to limited work or exiting the workforce.

Minor Disability Structured Settlements

Minor disability structured settlements involve claims in which a child receives compensation for an injury or medical negligence. Courts typically require structured payouts to protect funds until adulthood. Payment schedules often release funds at specific ages or milestones to support education and care.

Custom or Hybrid Structured Settlements

Custom or hybrid structured settlements combine periodic payments and future lump sums. These arrangements address unique financial needs such as planned surgeries, education costs, or housing expenses. Settlement terms are tailored during negotiations to match the recipient’s long-term financial outlook.

Structured Settlement Payment Options

Structured settlements are flexible. They can be designed to meet custom needs. The payment schedule is built based on the claimant’s medical needs, living expenses, and long-term plans. Below are the most common payment options.

Monthly Payments

Monthly payments are the most common option. They act as a steady paycheck and are ideal for ongoing living costs, monthly medical bills, and day-to-day expenses. This option is best when the claimant needs a consistent income over time.

Annual Payments

Annual payments work like a yearly financial boost. They are often used when medical costs are predictable or when the claimant needs a lump-sum payment once a year for major expenses such as rent, taxes, or insurance.

Lump Sum Payments

Lump sum payments give the claimant immediate access to the full settlement amount. This option is rare in structured settlements because it defeats the purpose of long-term financial protection. Still, some cases include a lump sum component alongside periodic payments.

Deferred Payments

Deferred payments start after a set period. This option is commonly used when future costs are expected, such as upcoming surgeries, education, or long-term care. Payments begin when the claimant needs the money most.

Hybrid Payment Structures

Hybrid structures combine different payment options. For example, a case might include monthly payments plus a deferred lump sum for future medical needs. This is often used when the claimant has both short-term and long-term financial needs.

Advantages of Structured Settlements

Structured settlements offer several concrete benefits that make them more than just an alternative to a lump sum. These advantages manifest in financial security, long-term planning, and outcomes for many recipients.

Guaranteed Income Over Time

Structured settlements are designed to provide a predictable schedule of periodic payments instead of a one-time payout. This setup gives recipients a steady income stream that can cover medical costs, living expenses, and future needs. Long-term income helps people avoid the risk of spending large sums too quickly, a concern often seen with lump sum awards.

One survey found that more than 90% of structured settlement annuity recipients reported feeling financially secure after choosing periodic payments rather than a lump sum. Additionally, 79% said their standard of living improved once regular payments began, and 76% felt more confident about their financial choices after structured payments began.

Tax Efficiency Under Federal Law

Structured settlement payments from physical injury or wrongful death claims are usually exempt from federal income tax under U.S. tax law. This benefit comes from the Periodic Payment Settlement Act of 1982 and Internal Revenue Code Section 104(a)(2), which allows compensation received for personal physical injuries or sickness to be tax-free.

Tax exemption means recipients retain more of their settlement amount over time than they might with taxable income or investment returns on a lump sum.

Long-Term Financial Security and Peace of Mind

Structured settlements help protect against premature depletion of settlement funds. Historical industry research shows that a significant percentage of lump-sum recipients spend settlement money much faster than expected, sometimes within a few years. Structured payments reduce this risk by pacing funds over time to meet long-term needs.

This security can help individuals focus on recovery and planning rather than constantly worrying about running out of money.

Customizable Payment Schedules

Structured settlements are not one-size-fits-all. Payment schedules can be customized to fit specific financial goals and life milestones. Some plans include monthly payments. Others are designed to increase over time, or to include larger amounts at key life stages, such as education or retirement. This flexibility allows claimants to align future income with costs.

Protection Against Financial Mismanagement

Receiving a large lump sum can be difficult to manage, especially for people without financial planning experience. Historical data suggest that many lump-sum settlement recipients spend their money faster than expected, often leaving them without resources a few years later. Structured settlements help mitigate this risk by spreading payments over time, reducing the likelihood of premature depletion.

Disadvantages of Structured Settlements

Structured settlements offer stability, but they are not perfect for everyone. These arrangements trade flexibility and immediate access for long-term consistency. It is important to understand the downsides before choosing this option.

Limited Access to Funds

Once a structured settlement is established, the recipient cannot easily access a large cash sum. Payments follow a fixed schedule, and there is no built-in option for early withdrawal. If unexpected costs arise, this lack of liquidity can feel restrictive and delay critical financial decisions.

Inflexibility of Payment Terms

Structured settlements are designed to follow specific payment terms. After the agreement is finalized and approved, changing the schedule or amounts is rarely possible. This limitation can be challenging when financial needs evolve over time, such as new medical costs or family expenses.

Risk of Inflation Eroding Value

Most structured settlement payments are fixed over time. If inflation increases significantly, the purchasing power of periodic payments can decline. Unless inflation adjustments are included in the original terms, this risk can reduce the real value of future income.

Opportunity Cost of Fixed Payments

Structured settlements provide guaranteed income, but they do not offer investment growth potential. If a lump sum had been invested wisely, it could yield higher returns. Recipients give up that opportunity when they choose structured payments.

Dependence on Insurance Company Stability

Structured settlements are funded through annuities issued by insurance companies. The reliability of future payments depends on the insurer’s financial stability. While rare, financial trouble at the insurance company could affect payouts and create uncertainty.

Selling Often Comes at a Discount

If a recipient needs immediate cash, selling future payments is possible, but it typically involves a discount. That means the lump sum received from selling will be significantly less than the total value of future payments. Court approval is also required for these sales, adding complexity.

Legal Structure of Structured Settlements

Structured settlements exist because U.S. law created a clear legal and tax framework that makes periodic payments preferable to lump sums in many physical injury cases. The rules control how settlements are funded, taxed, and enforced, and they differ from typical financial arrangements.

Statutory Basis and Key Tax Codes

The use of structured settlements in the United States gained formal legal backing with the Periodic Payment Settlement Act of 1982 (Public Law 97-473), which encouraged long-term payment arrangements in personal injury cases.

Under the U.S. Tax Code, structured settlements must meet specific requirements in Internal Revenue Code Sections 104(a)(1), 104(a)(2), and 130 to receive tax-favored treatment. These sections collectively govern which damages qualify for exclusion from income and how settlement payment obligations are treated for tax purposes.

Section 104(a)(2) allows damages received on account of physical injury, sickness, or wrongful death to be excluded from gross income for federal tax purposes. This applies whether payments are received all at once or over time. Section 104(a)(1) covers workers’ compensation payments that are also excludable from income.

Section 130 addresses how annuity obligations are assigned and funded so that insurers or qualified assignment entities can assume periodic payment obligations without treating the settlement funds as taxable income.

Qualified Assignment and Annuity Funding

In a structured settlement arrangement, the defendant or their insurer typically assigns periodic payment obligations to a qualified assignment company. That company then purchases an annuity from a life insurance company or an equivalent funding asset to guarantee future payments.

This step ensures payments are secured and meet the code’s requirements for scheduled amounts and timing. Under tax rules, the obligation assumed through a qualified assignment must be fixed, not alterable by the recipient, and payable by a party to the suit or someone assuming liability under Section 130.

Legal Definitions in the U.S. Code

The statutory definition of a structured settlement appears in 26 U.S.C. § 5891, which defines a structured settlement as an arrangement established by a lawsuit or agreement in which damages are excludable from income and paid periodically under terms described in the Internal Revenue Code. The same section defines structured settlement payment rights and outlines how transfers or factoring transactions are treated under the law.

Court Approval and Oversight

Many jurisdictions require court approval for structured settlements, especially when minors or legally incapacitated individuals are involved. Court oversight ensures that the payment schedule is reasonable and in the claimant’s best interests, protecting recipients from agreements that could compromise long-term security. While not always codified in federal law, this requirement exists in state structured settlement protection acts and common practice.

Can You Sell a Structured Settlement?

Structured settlements can be sold, but the process is controlled and regulated. The sale must be approved by a court. Courts review the offer to ensure the deal is fair, legal, and in the recipient’s best interests.

Selling a structured settlement is not a “simple cash-out.” It involves paperwork, legal approval, and a trusted buyer. You should sell structured settlement to buyers who’re court approved and follow legal compliance. MySettlement has been the first choice of sellers for over 20 years.

Is Selling a Structured Settlement Legal?

Yes. You can sell a structured settlement legally in most U.S. states, but it requires court approval. The court checks the deal under the Structured Settlement Protection Act (SSPA).

This law exists to protect recipients from unfair deals and financial exploitation. The court’s job is to make sure you’re not being pressured or misled.

When Selling Makes Sense

Selling makes sense when you need a large lump sum for a financial need. Common reasons include:

- Medical bills

- Mortgage or debt payoff

- Education expenses

- Starting a business

- Major life events or emergencies

If the future payment stream doesn’t match your immediate needs, selling can help you take control of your cash flow.

When Selling May Not Be Ideal

Selling may not be ideal if you rely on those future payments for basic living expenses.

If you have a steady income and no urgent financial need, keeping the structured settlement often makes more sense.

Also, selling means you will receive less than the total value of your future payments. The buyer must profit, so the lump sum will always be discounted.

How Selling a Structured Settlement Works

Selling a structured settlement follows a set process. You request a quote, the buyer evaluates the case, the court reviews the deal, and then you receive your lump sum once approved.

Requesting a Quote

You start by submitting your settlement details. This includes your payment schedule, court order, and the amount you receive.

The buyer reviews your information and prepares a cash offer. This step is usually fast, and you can do it online or over the phone.

Quote Approval Process

Once you accept the offer, the buyer starts the legal approval process.

This includes court filings and documentation. The judge will evaluate the deal’s fairness and ensure it benefits you.

Approval times vary by state, but the process typically takes a few weeks.

Receiving Your Lump Sum

After the court approves the sale, the buyer purchases your future payments.

You receive your lump sum via bank transfer or check. The payments stop, and the buyer takes over the future payment stream.

Tax Implications of Selling a Structured Settlement

In most cases, selling a structured settlement does not trigger federal income tax, but the tax outcome depends on how the original settlement was structured and why it was awarded.

Federal Tax Treatment (Clear Explanation)

Under Internal Revenue Code (IRC) Section 104(a)(2), structured settlement payments that originate from personal physical injury or physical sickness claims are excluded from gross income. This tax-free status generally continues even if the recipient sells future payments for a lump sum.

In simple terms:

- If your structured settlement payments were tax-free when received periodically,

- They are typically tax-free when sold, because the sale does not change the character of the original income.

The IRS views the transaction as an assignment of payment rights, not as newly generated taxable income.

Important Exceptions to Be Aware Of

Selling a structured settlement may have tax consequences in certain situations, including:

- Non-physical injury settlements

Payments related to emotional distress, employment disputes, or punitive damages may be taxable, whether received over time or sold. - Interest or investment-based components

If part of the settlement includes taxable interest or earnings, that portion may be subject to tax upon sale. - State-level tax treatment

While federal law governs income tax exclusion, state tax rules can vary, and some states may treat lump-sum proceeds differently. - Improperly structured settlements

If the original settlement was not compliant with IRC Sections 104(a)(2), 130, or 5891, tax protection may be limited.

Why Professional Advice Still Matters

Although most sellers owe no federal income tax, individual circumstances differ. Factors such as:

- the nature of the original claim,

- the settlement agreement language, and

- state tax laws

can affect the final outcome.

For this reason, it is generally advisable to consult a tax professional or settlement advisor before selling, especially for high-value settlements or complex cases.

History of Structured Settlements in the United States

Structured settlements were formally adopted in the United States during the 1970s, though their conceptual origins trace back to Canada in the 1960s, following mass injury claims caused by the drug thalidomide. In those cases, courts recognized that severely injured claimants, many of them children, required long-term financial support, not a single lump-sum payout that could be quickly depleted.

As similar catastrophic injury cases emerged in the U.S., structured settlements became a practical solution for aligning compensation with future medical care, rehabilitation costs, and lifetime living expenses.

A major turning point came in 1979, when the IRS issued Revenue Ruling 79-220, clarifying that periodic payments received from qualifying personal injury settlements were excluded from gross income. This ruling established the federal tax foundation that made structured settlements financially attractive and legally viable.

Congress reinforced this framework with the Periodic Payment Settlement Act of 1982, which formally integrated structured settlements into federal law and prevented state taxation of qualifying payments. This legislative support accelerated court adoption throughout the 1980s, particularly in personal injury, wrongful death, and minor cases.

Subsequent legislation, including the Small Business Job Protection Act of 1996, narrowed tax exclusions to damages arising from personal physical injury or physical sickness, further refining the application of structured settlements.

Today, structured settlements are a court-approved, federally regulated compensation mechanism, widely used to protect injury victims, reduce litigation risk, and ensure long-term financial stability.

Frequently asked questions

What is a structured settlement?

A structured settlement is a legal arrangement where compensation from a lawsuit is paid out over time instead of all at once. Payments are typically funded through an annuity issued by a highly rated life insurance company and are commonly used in personal injury, wrongful death, and workers’ compensation cases.

Are structured settlement payments guaranteed?

Yes, payments are contractually guaranteed under the terms of the settlement and backed by the issuing insurance company. While not federally insured like bank deposits, they are considered highly reliable due to the strict regulation of insurance carriers.

Can structured settlement payments be changed?

The original payment schedule cannot be modified unilaterally. However, recipients may choose to sell some or all future payments through a court-approved transfer if financial circumstances change.

Is selling a structured settlement legal in all states?

Yes, selling a structured settlement is legal in every U.S. state, provided the transaction complies with that state’s Structured Settlement Protection Act (SSPA) and receives court approval confirming the sale is in the seller’s best interest.

Do I have to sell all my payments?

No. Many people choose to sell only a portion of their future payments—such as a few years’ worth or a single lump payment—while keeping the rest of the settlement intact.

How long does it take to sell a structured settlement?

Most transactions take 30 to 90 days, depending on state court requirements, document availability, and judicial scheduling. Faster timelines are possible in some jurisdictions.

Will selling my structured settlement affect my taxes?

In most cases, selling payments does not create new federal income tax liability, but individual circumstances vary. Consulting a qualified tax professional is strongly recommended before proceeding.

How do I know if a buyer is legitimate?

Reputable structured settlement buyers are transparent about pricing, comply fully with court requirements, and never pressure you into selling. Court oversight exists specifically to protect recipients from unfair or predatory transactions.

Conclusion

Structured settlements were designed to do one thing well: protect long-term financial stability after life-altering events. Backed by federal law, court oversight, and decades of legal precedent, they remain one of the most reliable compensation structures in the U.S. legal system.

At the same time, life does not always unfold according to a payment schedule written years earlier. When priorities shift—medical needs change, opportunities arise, or financial pressure builds—the ability to sell a structured settlement legally and responsibly gives recipients flexibility without dismantling the protections courts originally intended.

The key lies in understanding how structured settlements work, knowing your legal rights, and working with experienced professionals who prioritize transparency and compliance over speed or sales pressure.

Informed decisions—not rushed ones—are what turn a structured settlement into a tool that truly serves you, both now and in the future.

This article is for general informational purposes only and does not constitute legal, tax, or financial advice. Consult a qualified professional before making any decisions about your settlement payments.

Your settlement has a number. Let's make it work for you.

Get a free, no obligation quote from a specialist who actually knows what your payments are worth.